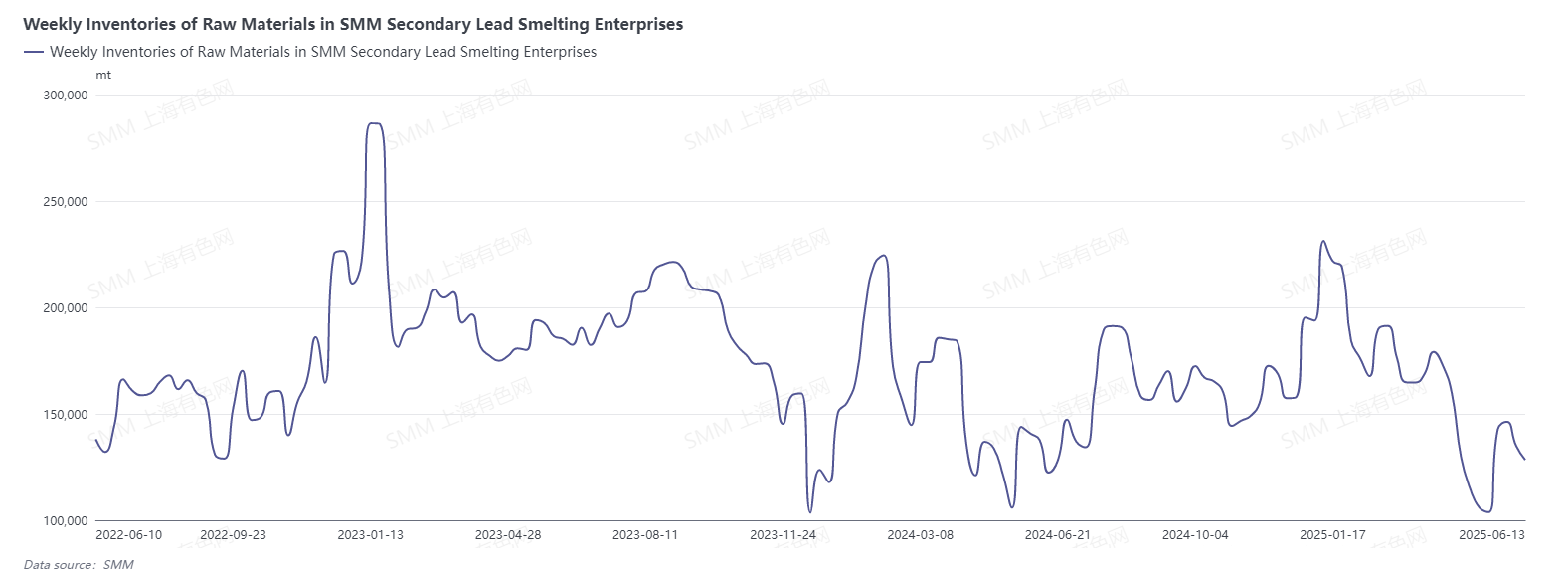

Currently, the amount of waste lead-acid batteries being scrapped in China remains tight. Multiple recyclers have indicated that the daily average collection volume has declined by approximately 50% compared to the period from April to May. The same trend is observed in the arrivals at secondary lead smelters. According to a large enterprise in Central China, the daily average arrivals of waste batteries last month were around 40 trucks, while this month, the daily average arrivals are only around 15 trucks. As can be seen from the chart below, the weekly inventory of raw materials has continued to decline since 2025.

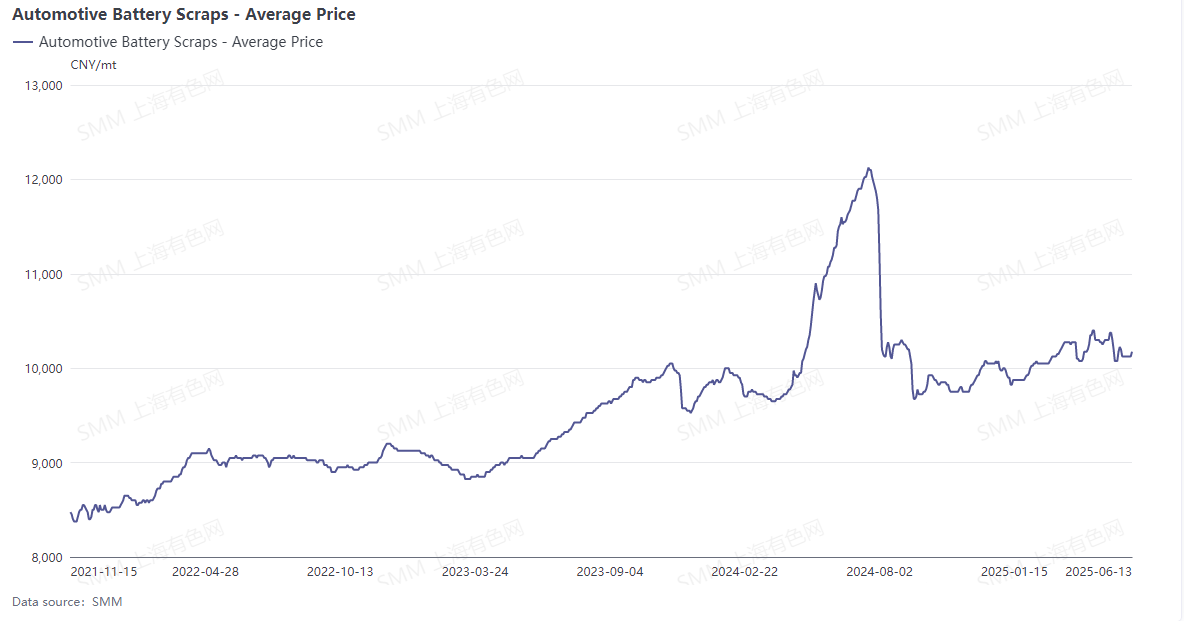

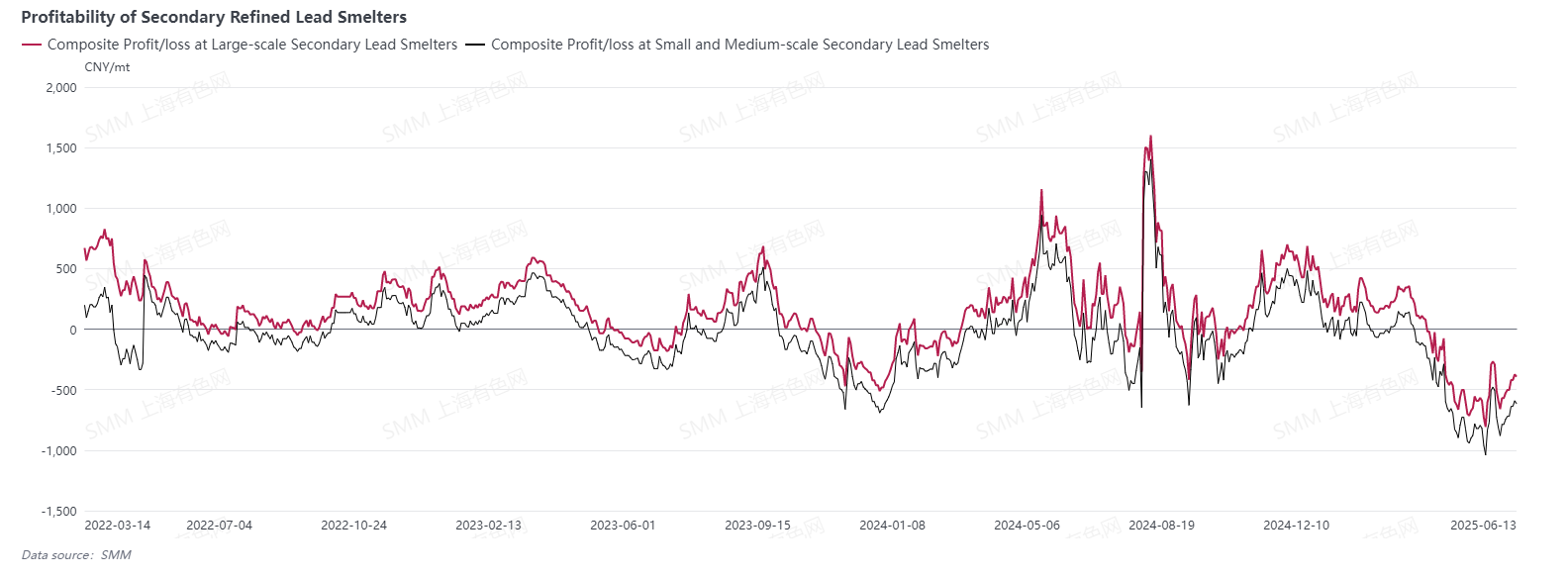

Due to tight supply of raw materials and intense competition among smelters, the prices of scrap batteries remained strong. Meanwhile, downstream battery producers showed low enthusiasm for purchasing lead ingots, and lead prices were in the doldrums. Smelters suffered significant losses, and in late May, several smelters called for a sharp drop in the purchase quotes for scrap batteries. At that time, the prices of waste EV batteries plunged by 500 yuan/mt daily, and some smelters in certain regions followed suit by reducing their quotes by 200 yuan/mt, leading to chaotic market quotes. Collection stores and recyclers of waste lead-acid batteries, fearing further price drops, sold off their stocks. However, due to limited market supply, after a period of selling, smelters once again faced poor arrivals. Some enterprises saw their purchase quotes rebound. As of last week, the differences in quotes among enterprises had largely returned to normal. Currently, the mainstream tax-inclusive prices of waste EV batteries hover around 10,200-10,250 yuan/mt.

According to some enterprises, despite the increase in procurement quotes, the arrivals of raw materials remain unpromising. To enhance procurement competitiveness, individual enterprises have adopted a point-to-point quoting model, offering different settlement prices based on different recyclers and quantities of reported goods. With such competitive pressure compounded by the lead price's struggle to rise, smelters continue to operate at a loss.

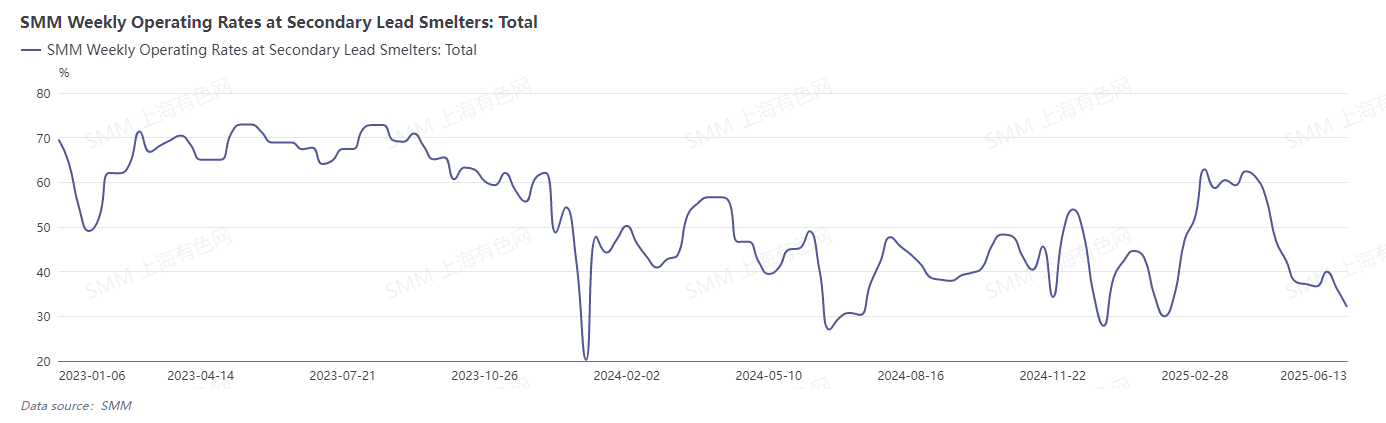

At present, secondary lead smelters are only producing to fulfill long-term contracts, and the "more production, more losses" situation has dampened their production enthusiasm. Some small enterprises even prefer to purchase lead ingots from other companies to fulfill long-term contracts rather than producing on their own. The weekly comprehensive operating rate of secondary lead smelters has dropped to nearly 30%; enterprises are experiencing a "dire" predicament.